Family money can feel like a constant stream of small decisions, because you are not only paying bills, you are also funding routines, growth, surprises, and the everyday needs of people who change fast.

This guide gives you simple budget categories for families that are concrete enough to track, flexible enough to adapt, and easy to label in an app or spreadsheet without turning budgeting into a second job.

Simple budget categories for families: why categories matter more than you think

Categories are not just labels, because the way you group spending determines what you notice, what you ignore, and what you can realistically improve.

Parents often feel like money disappears because household spending is spread across groceries, school needs, subscriptions, appointments, and last-minute kid requests that arrive at the worst timing.

Clarity reduces stress quickly, because a clear category list turns chaos into a map, and a map makes it easier to choose trade-offs without guilt.

Flexibility matters in family life, because kids have seasons, schools have calendars, and your household needs can change without warning.

Simplicity protects consistency, since a category system that is too detailed will be abandoned during busy weeks when you most need it.

Useful categories strike a balance, because they are specific enough to guide behavior yet broad enough to keep tracking manageable.

What “simple” should mean for a family budget

Simple should mean you can review your categories in ten minutes, because parents rarely have unlimited time for financial admin.

Simple should also mean your categories match how you actually spend, because budgeting works when it reflects real life rather than an ideal life.

Simple does not mean ignoring important costs, since the quickest way to feel like your budget “fails” is to forget predictable family expenses.

How to decide whether to combine or split a category

A category should be split when two different behaviors are hiding inside one number, because you cannot improve what you cannot see clearly.

A category should be combined when tracking becomes annoying, since annoyance is often the early signal that your system is too complicated.

Family budgeting often improves when you split groceries from dining out, because food spending has different triggers depending on whether you are shopping or outsourcing meals.

Household spending becomes easier when you combine tiny, low-impact items into one “household essentials” bucket, because you avoid micromanaging paper towels like they are a moral issue.

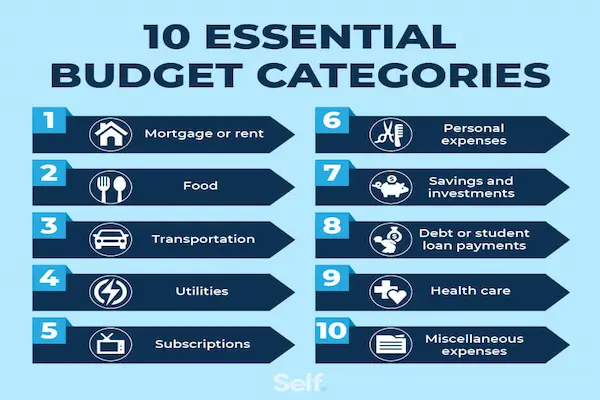

Start here: the simplest family budget category structure that still works

If you feel overwhelmed, start with broad buckets, because broad buckets create momentum and prevent the “I never finished setting it up” problem.

This starter structure is designed for parents managing most shared bills and kid-related costs, so the big picture becomes visible quickly.

The 6-bucket starter system

- Shared bills, covering the fixed obligations that keep the household running.

- Household essentials, covering groceries and day-to-day basics that change each week.

- Kids, covering school and child-related costs that pop up frequently.

- Transportation, covering commuting and family mobility.

- Health, covering medical, dental, prescriptions, and wellness needs.

- Savings and goals, covering emergency buffer, sinking funds, and future plans.

That structure works because it captures the major flows of family money, while leaving room to expand into more detail when you are ready.

When to expand from 6 buckets to 12–18 categories

Expansion makes sense once you are checking your budget weekly, because detail helps only when you look at it regularly.

More categories can help when one bucket is consistently over, since splitting that bucket can reveal the real driver behind the overspending.

Growth is best done slowly, because adding five categories at once often creates friction and then avoidance.

Simple budget categories for families: the full list you can copy

The categories below are organized by purpose, so you can copy them into your budgeting app or spreadsheet and then remove anything that does not apply.

Names are intentionally plain, because simple labels reduce confusion when you are categorizing transactions quickly.

Shared bills categories for stable household basics

- Mortgage / Rent (or “Housing Payment”), because shelter is the foundation of every other plan.

- Electricity, because this bill can vary and deserves its own line in many households.

- Water / Trash, because municipal services can be predictable yet still important to track.

- Gas / Heating, because seasonal spikes are easier to manage when you see them clearly.

- Internet, because connectivity is often essential for work, school, and family communication.

- Mobile Phones, because family plans can grow over time and sometimes hide upgrades.

- Streaming / Subscriptions (optional separate line), because subscription creep is common in busy households.

- Insurance (Home / Renters), because protection costs are part of stability.

- Insurance (Auto), because vehicles often represent a major family expense and risk area.

- Insurance (Health) (if not deducted from paychecks), because healthcare costs deserve visibility.

Household essentials categories for everyday living

- Groceries, because food at home is a major driver of household spending.

- Household Supplies, because cleaning items, paper goods, and basics are real recurring costs.

- Dining Out / Takeout, because convenience meals are usually the first category to drift in busy seasons.

- Pet Care (if relevant), because food, vet visits, and supplies add up like kid costs do.

- Clothing (Family), because kids grow and weather changes rarely wait for the budget to feel ready.

- Home Maintenance, because small repairs happen and large repairs happen eventually.

- Home Improvement (optional separate line), because projects can quietly expand if they are not tracked.

Transportation categories that keep the family moving

- Fuel, because gas spending responds to routines and schedule shifts.

- Public Transit (if relevant), because passes and fares can be managed with clear targets.

- Car Payment (if applicable), because it behaves like a fixed bill that shapes monthly flexibility.

- Car Maintenance, because tires, oil changes, and repairs are predictable irregular expenses.

- Parking / Tolls, because these small fees can add up quietly across a month.

- Rideshare / Taxi (optional), because this is often a convenience upgrade that families want visible.

Health categories for predictable and unpredictable care

- Prescriptions, because recurring medication costs are easier to plan for when they are visible.

- Doctor / Clinic, because copays and visits can pop up with little warning.

- Dental, because cleanings and orthodontics can become major family budget lines.

- Vision, because glasses and contacts can be irregular yet expected.

- Mental Health, because therapy or support services can be essential and deserve planned funding.

- Health Supplies, because first-aid, vitamins, and basic supplies are common household needs.

Kids expenses categories that reflect real family life

Kids expenses are often the reason a parent feels financially overwhelmed, because they arrive in bursts around school calendars, growth spurts, and social life.

Keeping kid-related spending visible reduces surprise, because visibility helps you plan ahead and makes it easier to say yes to what matters.

- Childcare / Daycare, because this is often one of the largest predictable family costs.

- School Costs, because supplies, fees, and class needs appear throughout the year.

- Lunches / School Meals (optional), because separating it can help if school food is a regular expense.

- Activities / Sports, because fees, uniforms, equipment, and travel can add up quickly.

- Lessons, because music, tutoring, or specialized coaching often comes with monthly costs.

- Kids Clothing (optional split), because growth and seasonal shifts can drive frequent purchases.

- Kids Medical (optional split), because kid care can have unique costs like braces or specialists.

- Kids Fun, because small treats, movies, and weekend activities are real and deserve a plan.

- Birthday Parties / Gifts, because social obligations are predictable and easier with a sinking fund.

- Baby Supplies (if relevant), because diapers and formula behave like essentials and can be significant.

Shared bills vs kids expenses: a quick decision guide

- Put school tuition under Kids, because it is tied to your child rather than your home.

- Put internet under Shared bills, because it supports the whole household and behaves like a fixed monthly cost.

- Put groceries under Household essentials, because it serves the family but behaves like a flexible category.

- Put daycare under Kids, because it is child-specific and often a major line worth tracking clearly.

Household spending categories that reduce day-to-day chaos

Household spending tends to include many small purchases, so category design should protect your time and your sanity.

- Household Essentials as a combined category can work, because it keeps tracking fast when life is busy.

- Home + Garden can be a single bucket, because seasonal purchases are common and hard to separate perfectly.

- Convenience Spending can be helpful, because delivery fees, rush purchases, and “we forgot” items show a clear pattern.

How to label categories in budget apps or spreadsheets

Labels should be easy to read at a glance, because you will be categorizing quickly and reviewing totals under time pressure.

Short names reduce mistakes, since long names tend to get truncated or confused inside apps.

Consistent naming makes reports useful, because you can compare months without wondering whether “Food” and “Groceries” were meant to be the same.

Category label examples you can copy exactly

- Housing: Rent

- Housing: Repairs

- Bills: Electric

- Bills: Water/Trash

- Bills: Internet

- Bills: Phones

- Food: Groceries

- Food: Dining Out

- Transport: Fuel

- Transport: Maintenance

- Kids: Childcare

- Kids: School

- Kids: Activities

- Kids: Fun

- Health: Prescriptions

- Health: Appointments

- Goals: Emergency Fund

- Goals: Sinking Funds

Two naming systems that stay organized as life changes

A prefix system keeps your list tidy, because related categories stay grouped together in alphabetical lists.

A section system works too, because some apps allow you to create groups like “Bills” and “Kids” with categories inside.

- Prefix style: “Kids: Activities” and “Kids: School” stay together when sorted.

- Section style: “Kids” section contains “Activities,” “School,” and “Clothing.”

Combining and splitting: practical examples for real family life

Families often start too detailed, then quit, so it helps to know which categories are worth splitting and which are worth combining.

Choosing splits strategically improves clarity without increasing workload too much.

Categories worth splitting for most families

- Groceries vs Dining Out, because one is essentials and the other is often schedule-driven convenience.

- Kids School vs Kids Activities, because these costs follow different seasons and different triggers.

- Car Payment vs Car Maintenance, because the payment is fixed while maintenance is irregular and needs sinking fund planning.

- Home Maintenance vs Home Improvement, because repairs are often required while improvements are often optional and can expand.

- Health Insurance vs Out-of-Pocket Care (if not payroll-deducted), because premiums and visits behave differently.

Categories often better combined for simplicity

- Household Supplies + Toiletries, because separating soap from paper towels rarely improves decisions.

- Kids Fun + Family Fun (sometimes), because outings often include everyone and splitting costs can be exhausting.

- Small Subscriptions into one line, because tiny monthly charges can be tracked as a group if you review them periodically.

- School Fees + Supplies into “Kids: School,” because both are tied to school and usually move together.

A simple decision tree for category design

- Ask whether the spending is frequent and meaningful, because frequent meaningful spending deserves visibility.

- Ask whether the spending is irregular but predictable, because irregular predictable spending belongs in sinking funds or special categories.

- Ask whether separating it changes your choices, because categories should guide behavior rather than create busywork.

- Ask whether tracking it feels annoying, because annoyance is a signal to simplify.

Kids expenses: build “mini systems” that make kid costs predictable

Kid-related costs often arrive in bursts, so mini systems help you fund them gradually instead of scrambling.

Sinking funds are especially helpful for kids, because school years, birthdays, and activities happen on schedules you can anticipate.

Common kid-cost seasons and how to plan categories around them

- Back-to-school season often includes supplies, clothes, and fees, so a “Kids: School” sinking fund can reduce stress.

- Sports and activities season</strong often includes registration, equipment, and travel, so “Kids: Activities” works best with a monthly set-aside.

- Birthday party season</strong can become expensive quickly, so “Kids: Gifts/Parties” prevents last-minute budget blows.

- Growth spurts</strong can create surprise clothing needs, so “Kids: Clothing” can be a small but steady category.

Simple sinking fund ideas for families

- School supplies and fees, because these are predictable even when they vary by grade.

- Activity registrations, because sports and lessons often come in multi-month cycles.

- Holidays and gifts, because generosity is easier when it is planned throughout the year.

- Medical and dental, because braces and specialist visits can be costly and irregular.

- Home repairs, because every home needs maintenance and maintenance rarely arrives at a convenient time.

Shared bills and household spending: make responsibilities visible

One parent often ends up carrying the mental load of bills, so visibility can be as important as the categories themselves.

Clear ownership reduces forgotten payments, because “we both thought the other handled it” becomes less likely.

Shared clarity also reduces resentment, since invisible labor becomes visible when systems exist.

A simple responsibility map you can add to your budget

- List each fixed bill and its due date, because timing is part of household stability.

- Assign a primary owner for each bill, because one clear owner prevents confusion.

- Assign a backup checker, because families get sick and busy and need redundancy.

- Schedule a weekly 10-minute bill glance, because frequent small checks prevent late fees.

Bill category examples with ownership notes

- Mortgage / Rent — Owner: ___, Backup: ___, Due date: ___

- Electric — Owner: ___, Backup: ___, Due date: ___

- Internet — Owner: ___, Backup: ___, Due date: ___

- Insurance — Owner: ___, Backup: ___, Renewal month: ___

Practical tracking tips for busy parents

Tracking should be quick, because family life does not pause so you can perfectly categorize every receipt.

Weekly check-ins often work better than monthly surprises, because small adjustments are easier than big rescues.

Broad categories reduce friction, since you can always refine after the habit is established.

A 15–20 minute weekly family budget routine

- Check upcoming bills and due dates, because cash flow stress often comes from timing.

- Review groceries and dining out, because food spending is the category most families can influence quickly.

- Review kids spending categories, because school and activities often create quick surprises.

- Move money between categories if needed, because a living budget must adapt to real life.

- Write one short note about what changed, because notes make next month easier.

Three shortcuts that save time without losing clarity

- Use one combined “Household Essentials” category during busy seasons, because simplicity protects consistency.

- Create a buffer category, because it absorbs small surprises without forcing a full budget redesign.

- Split only the categories that keep going over, because targeted detail yields better results than universal detail.

Examples of “simple” family category sets at different complexity levels

Seeing complete sets helps you choose a level that fits your current season, because families have different time, energy, and complexity.

Level 1: Ultra-simple (8–10 categories)

- Housing

- Utilities

- Food (Groceries + Household)

- Dining Out

- Transportation

- Kids

- Health

- Savings / Goals

- Buffer

Level 2: Balanced (12–16 categories)

- Mortgage / Rent

- Utilities

- Internet + Phones

- Insurance

- Groceries

- Household Supplies

- Dining Out

- Transportation: Fuel

- Transportation: Maintenance

- Kids: Childcare

- Kids: School

- Kids: Activities

- Health: Out-of-Pocket

- Sinking Funds

- Savings / Goals

- Buffer

Level 3: Detailed but still family-manageable (18–25 categories)

- Housing: Rent/Mortgage

- Housing: Repairs

- Bills: Electric

- Bills: Water/Trash

- Bills: Gas/Heating

- Bills: Internet

- Bills: Phones

- Bills: Subscriptions

- Food: Groceries

- Food: Dining Out

- Household: Supplies

- Transport: Fuel

- Transport: Car Payment

- Transport: Maintenance

- Kids: Childcare

- Kids: School

- Kids: Activities

- Kids: Clothing

- Kids: Gifts/Parties

- Health: Prescriptions

- Health: Appointments

- Health: Dental

- Goals: Emergency Fund

- Goals: Sinking Funds

- Buffer

Common family budgeting problems and category fixes

Family budgeting problems often come from missing categories, unclear boundaries, or unrealistic expectations about how predictable kids can be.

Fixes usually work best when they adjust the system, because blaming willpower rarely helps busy parents.

Problem: groceries always blow up the budget

- Split groceries from household supplies, because supplies can spike in bulk-buying weeks.

- Add a weekly grocery target, because weekly numbers are easier to manage than monthly guesses.

- Create a “busy week meals” mini-plan, because schedule pressure often drives expensive convenience choices.

Problem: kids costs feel random and stressful

- Create a sinking fund for school and activities, because predictable bursts are easier when funded monthly.

- Split “Kids” into “School” and “Activities,” because those costs have different seasons and different controls.

- Add “Kids: Gifts/Parties,” because social obligations can be planned even when they feel spontaneous.

Problem: household repairs create panic every time

- Create “Home Maintenance” and fund it monthly, because small steady funding prevents big emotional hits.

- Keep a buffer line, because not every repair will fit neatly into the plan.

- Note the month repairs happened, because patterns help you predict timing over time.

Problem: you feel like you are doing all the budgeting alone

- Create a shared weekly check-in, because shared awareness reduces the mental load and increases teamwork.

- Assign bill ownership in writing, because written ownership prevents confusion and resentment.

- Agree on a small personal spending amount for each adult, because autonomy reduces the need to negotiate every purchase.

Important notes: education only, and independent content

This article is for general educational purposes only, and it is not financial, legal, or tax advice.

Every family has different income, debt, caregiving responsibilities, and costs, so adapt categories to your own reality and consider professional guidance if needed.

Notice: this content is independent and has no affiliation, sponsorship, or control over any institutions, platforms, or third parties mentioned.

Closing: categories create calm when family life feels expensive

Families do not need perfect tracking to benefit from a clear system, because the biggest relief often comes from simply knowing where money is going.

Simple budget categories for families work best when they reflect shared bills, household spending, and kids expenses in a way you can review weekly without dread.

As your family changes, your categories can change too, because budgeting is a living plan designed to support real life rather than control it.